Matt Arderne

Co-founder @ Sea.dev

Assessing a business’s financial health often depends on reviewing management financials and intermediary statements. The problem is that these rarely conform to a standard template.

This creates huge bottlenecks for lenders, who need to manually process these documents to get a clear picture of their risk exposure.

Our latest product update tackles this challenge head-on.

The Problem

My background is in industrial engineering and process optimization, and I’ve generally seen the following to be true:

- A complex process will have one bottleneck task, slowing the entire system.

- Until the bottleneck is removed, almost nothing else will improve the system.

- Improving other tasks can make things worse by overwhelming the bottleneck.

For SMB lenders, this bottleneck task is usually the issue of dealing with monthly management accounts or interim financial statements provided by borrowers.

The task of mapping these interim financials into an internal standard template (aka financial spreading) can reduce the efficiency of a team dramatically.

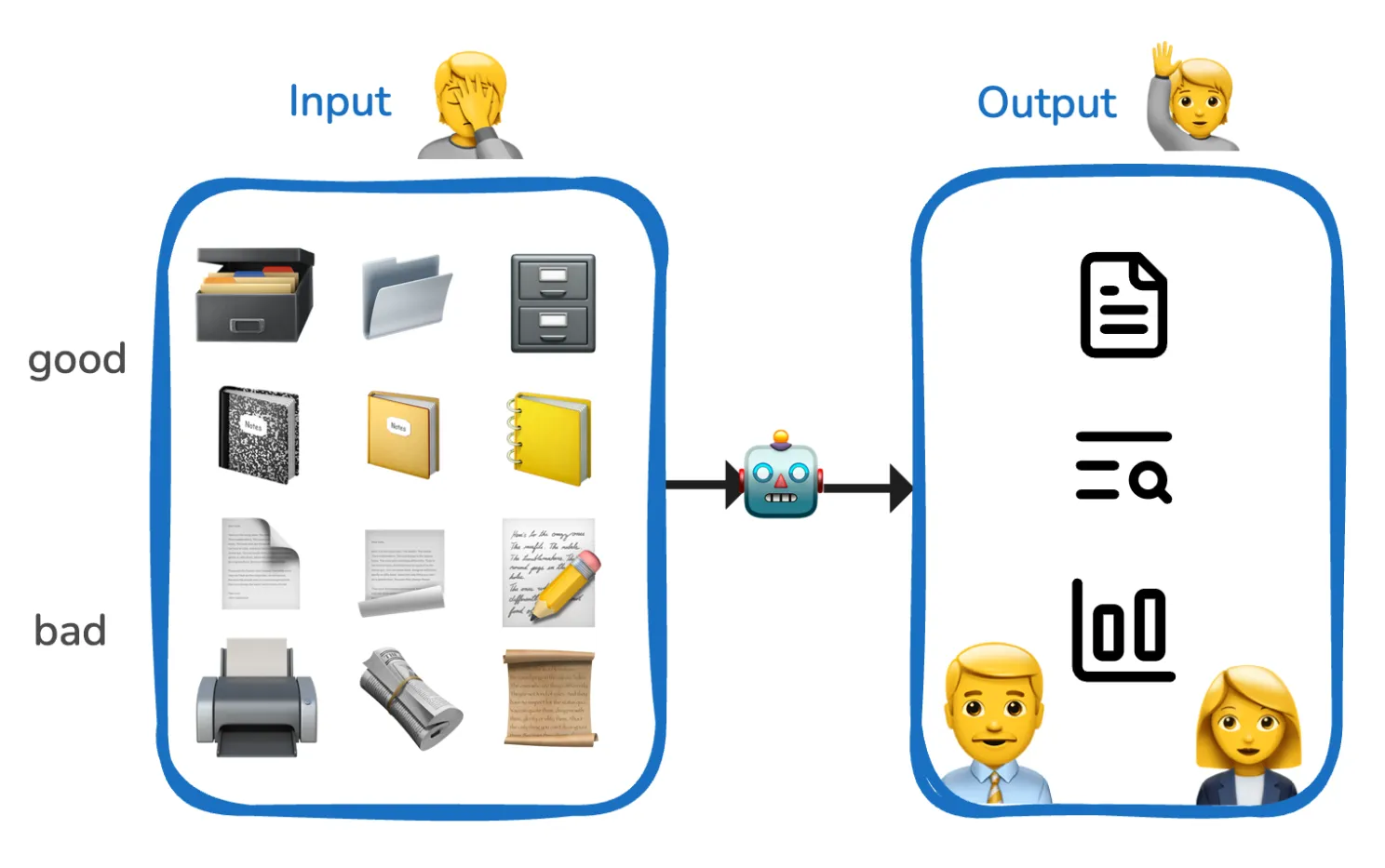

The reason? Interim financial statements do not conform to any template or standard, and are created by anyone from a financial director to an accountant or bookkeeper.

For documents matching an industry-standard format, traditional OCR tools are generally capable, but borrowers often can’t provide these.

The issues are varied:

- Formats can change month to month

- Corrections for prior months can be made without warning

- The person preparing them can change, leading to a completely overhauled process

These issues create a massive amount of work for lenders and a lack of visibility into company performance.

The Impact of the Problem

SMB lenders need to assess interim financial statements to get a real-time view of business performance.

Perhaps a regulatory change has impacted the company.

Typically, borrowers themselves don’t have visibility of their true month-to-month performance and rely on lenders to inform them about their financial standing and covenant clearance.

For lending programs like SBA loans, interim financials are required to check for changes between the start of the process and loan closing.

Today, most lenders deal with this by:

- Manually spreading the documents 🔴

- Using traditional OCR tools 🔴

- Outsourcing to lower-cost providers 🟠

- Avoiding by only doing simple loans 😵

At a certain scale, a bank can start to buy or build custom technology, but neither outsourcing nor legacy technology is particularly reliable:

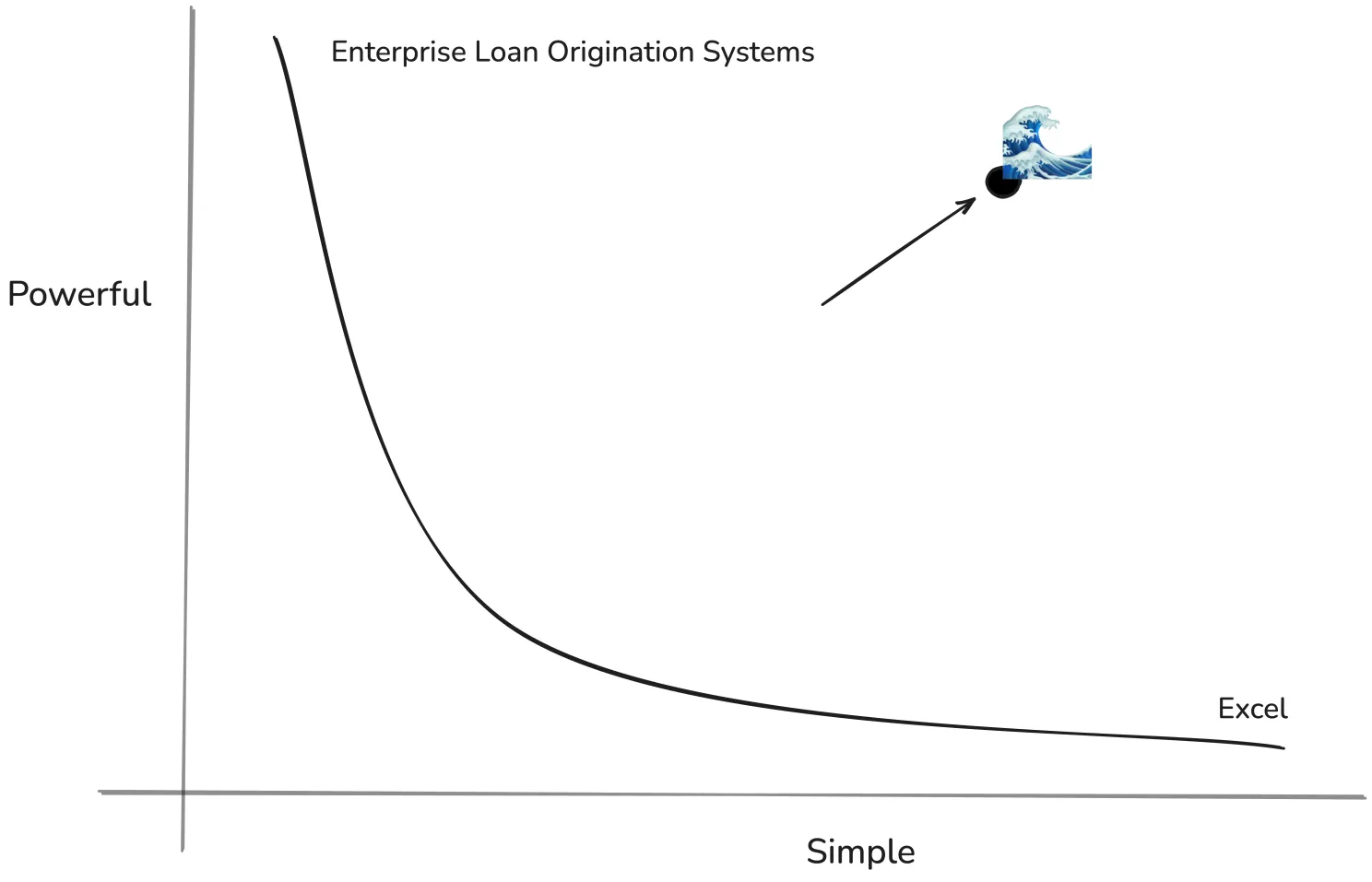

- Enterprise Loan Origination Software can automate simpler processes but is often complex and brittle.

- Outsourcing is just (costly) Excel—great for manual work but inefficient for workflow automation.

This is a complex problem for two reasons:

- On the input side → Statements can be extremely varied, often encompassing multiple companies.

- On the output side → Each lender has different target formats for covenant checks, with complex mapping nuances requiring a human to process effectively.

How We’ve Solved the Problem

Sea.dev is both Simple and Powerful.

We perfectly balance Powerful and Simple—enabling flexible software that lets users complete tasks quickly and adapt workflows easily.

Due to this flexibility, our Copilot AI is highly effective at financial document spreading, regardless of format.

This is enabled by the following features:

- Instantly create new assessment workflows → Users can flexibly spin up new workflows, removing constraints from legacy systems.

- Enhanced financial statement parsing → Our system now better understands non-standard financial statements, intelligently extracting data.

- Smart categorization → Financial data is automatically mapped into appropriate categories, improving accuracy and reducing manual work.

Each of these required engineering breakthroughs. We’ve found that combining intelligence, autonomy, and simplicity maximizes efficiency for financial analysis workflows.

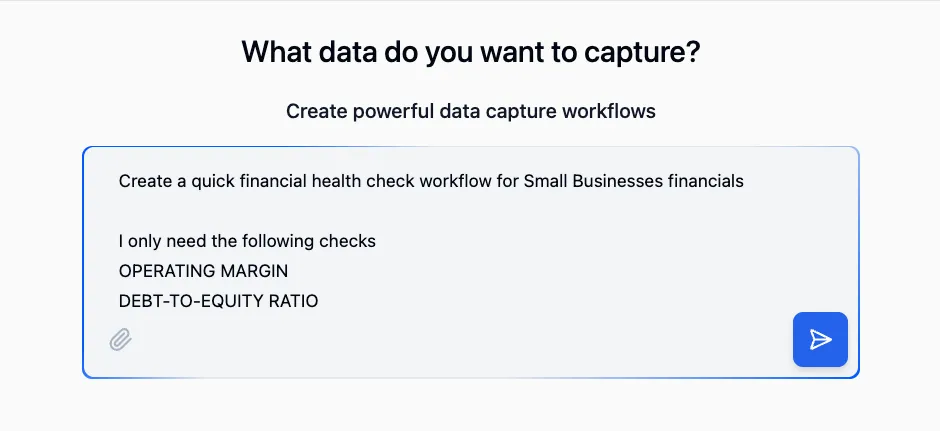

Example: How Simple It Can Be

- Describe the goal.

- Upload the latest management income statement and balance sheet with the instruction to check them against the lending criteria.

Simple. Two steps to a new assessment workflow.

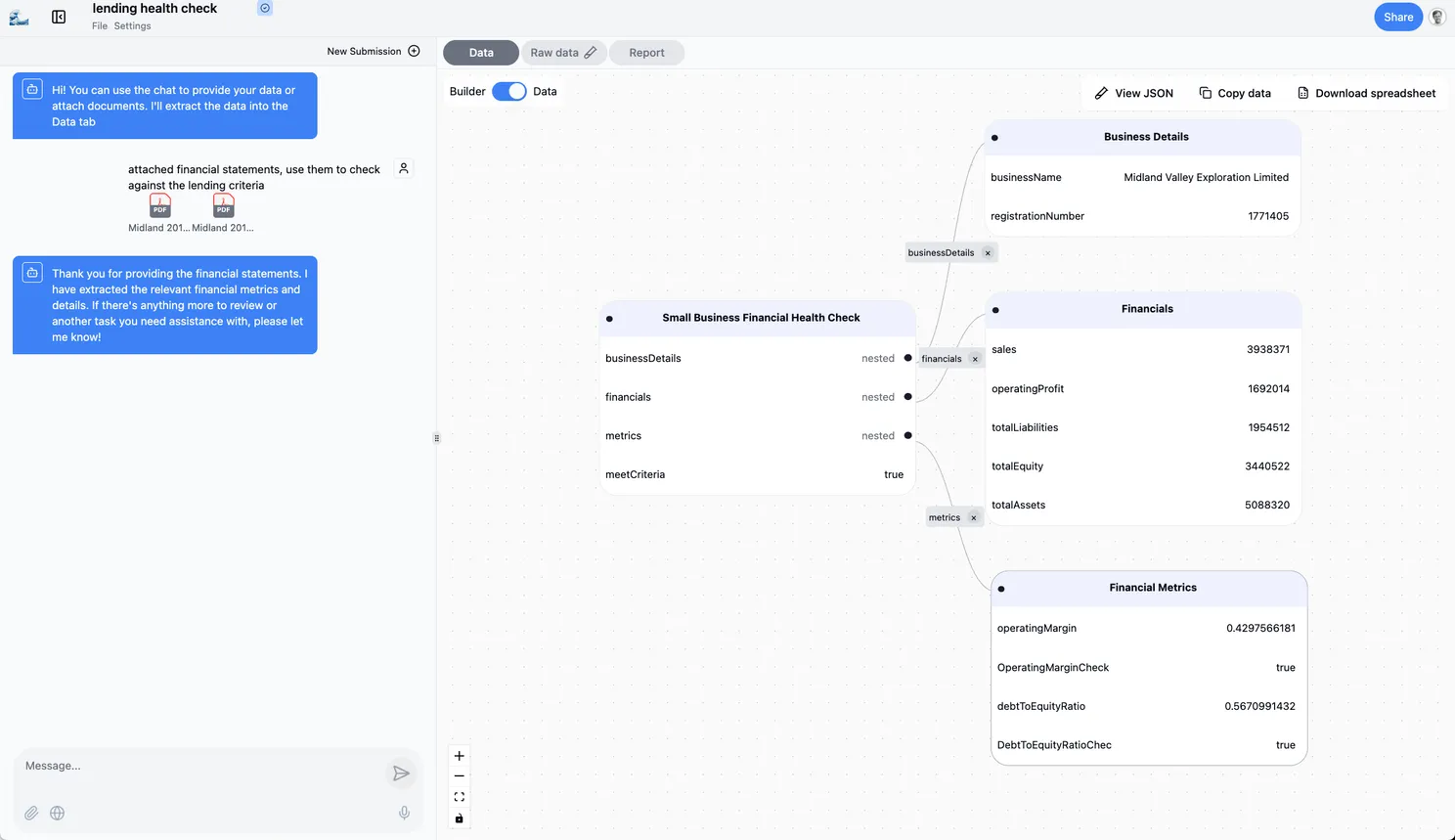

The company meets both the Operating Margin and Debt-to-Equity check.

On the backend, the full financials are processed and added to the deal room for deeper exploration, comparison, and referencing.

But to start, a basic health check is run, and the company passes.

Why This Matters

With these features, lenders and financial analysts can now:

✅ Spend less time manually entering data

✅ Make data-driven decisions faster

✅ Reduce the risk of errors in financial assessments

Next Steps

We’re working on SMB lending, SBA loans, and use cases requiring intermediary statements and business plans.

If you’d like to test this out or are interested in financial statement spreading, book a demo 🚀