Before we started Sea.dev, we tested every spreading solution on the market.

We tested solutions designed for enterprise banks. But we needed something different. Tools that could handle the variety of middle-market lending without forcing borrowers into rigid templates.

These tools were all excellent at what they were designed to do, but none of them worked for the complex loans we needed them for. Too big, too inaccurate, too tedious, or too expensive.

The discovery

Along this journey, we discovered what financial spreading actually involves. The combination of financial acumen, judgement calls, normalisation rules, and domain knowledge that turns messy source documents into clean, comparable financials.

The problem wasn’t just data extraction. It was the interplay between extraction, validation, normalisation, and analysis. Understanding what a “normal” expense looks like for a manufacturing company versus a SaaS business. Knowing when to reclassify a line item, when to add back a one-time charge, when to question a suspiciously round number.

The existing tools treated spreading like a mapping problem: get numbers from column A into column B. But spreading is a reasoning problem. An experienced analyst interprets, adjusts, reconciles, and defends their choices.

We rebuilt it from scratch.

Why spreading is so hard

The problem is this: spreading needs to be both consistent and flexible.

Consistent because you’re comparing companies across time and industries. Flexible because every business is different. Cash versus accrual, consolidated versus standalone, one-time events that distort trends.

Then add document variety: audited statements, reviews, compilations, tax returns, trial balances. Each with different reliability. And time pressure: deals move fast, underwriters need numbers today.

You can’t hire your way out of this.

Why we built an agentic solution from the ground up

After seeing what spreading actually required, we knew rule-based automation wouldn’t cut it. The variability was too high. The judgement calls too nuanced. The document formats too inconsistent.

We needed a system that could reason about financial statements the way an analyst does. Not just extract numbers, but understand context. Recognise when something looks off. Know when to apply an adjustment and when to leave things alone. Adapt to different industries, different accounting treatments, different deal structures.

We built an agentic, specification-driven approach. Our agentic loop plans before it acts, decomposes the work, and keeps cycling until the spec is satisfied. This delivers reliable spreading from messy inputs.

The SME Capital breakthrough

SME Capital had this exact problem. A portfolio growing towards hundreds of loans between £750,000 and £5 million. Every month, covenant monitoring and financial spreading ate up 35 analyst hours.

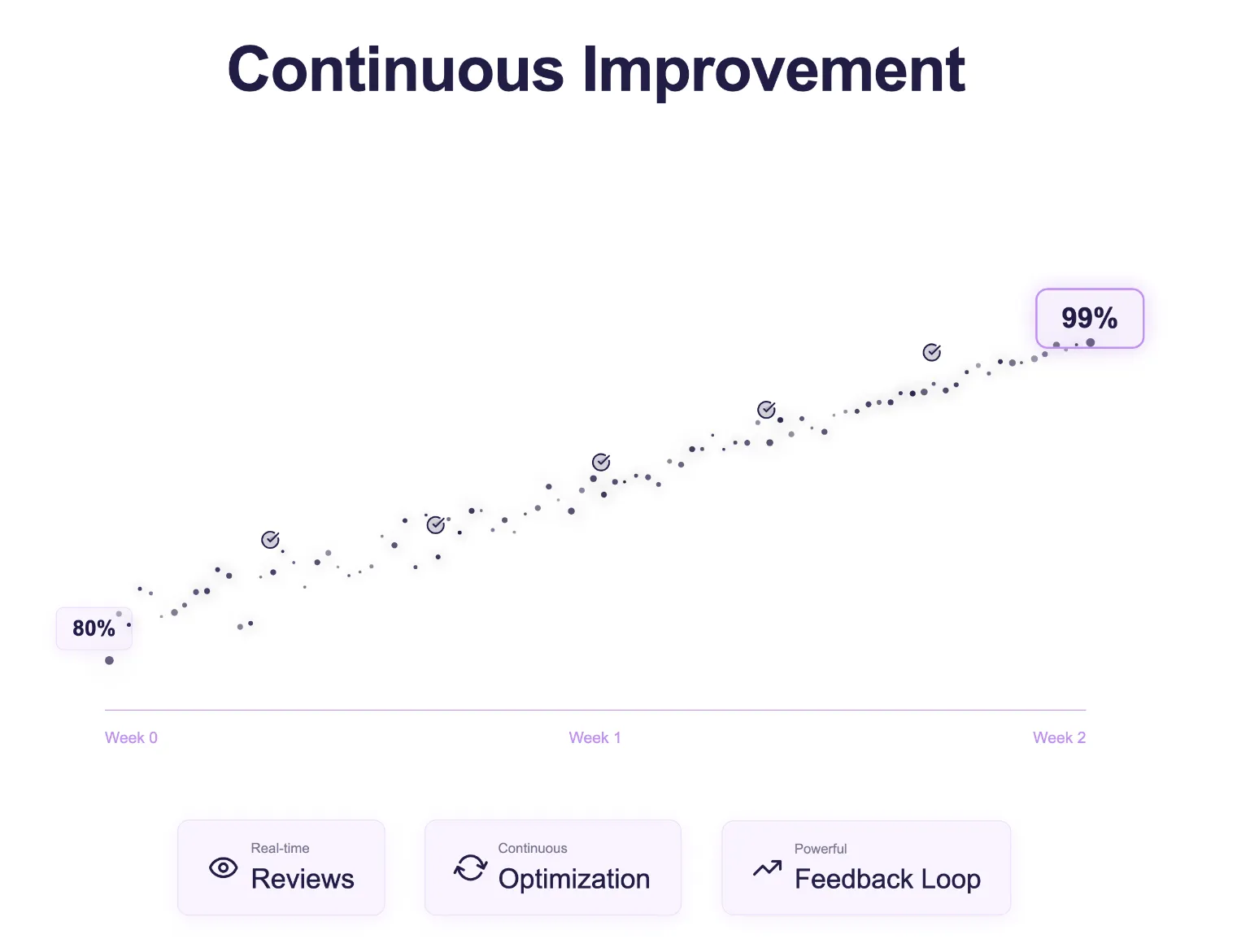

We deployed our system. Result: 35 hours down to 2 hours. A 94% reduction.

Monthly covenant monitoring that used to take a week now takes 2 hours. Thirty-three hours freed up every month. Those hours went straight to better understanding the businesses and building relationships.

The system started out with variable accuracy, but quickly hit 98% accuracy extracting financial metrics with human-in-the-loop feedback. Errors that led to missed covenant breaches have essentially disappeared. Covenant breaches get flagged in hours, not weeks. Management sees portfolio health in real time, not quarterly.

SME Capital needed to handle businesses with £250,000-plus earnings across manufacturing, distribution, and services. Each sector required different normalisation rules. Our specification-driven approach adapted to their credit philosophy, not the other way round. The agentic loop handles their entire portfolio refresh each month autonomously. Analysts log in at month-end, review the automated spreads, approve the clean ones, dig into the flagged cases. This human-in-the-loop approach creates a feedback cycle where every correction improves the system. The same people, same credit quality, but with 95% less manual work.

What we’re excited about for the future

Financial spreading is just the starting point. Once you have clean, normalised financials flowing automatically, the next layer becomes possible.

Predictive covenant modelling. Automated health scores. Real-time stress testing. Early warning systems that flag deteriorating borrowers before they miss a payment.

All of this depends on having reliable, normalised financial data at scale. That’s what automated spreading unlocks.

The future looks really interesting when it’s 100x cheaper to analyse financials. Think agentic analysis of real-time financials. Think continuous underwriting.

We’re building infrastructure for a new generation of portfolio management. Lenders spend time on judgement and relationships, not data entry. Risk monitoring is proactive. Growth isn’t limited by analyst capacity.

Testing every solution on the market before building our own taught us what actually matters: not features or integrations, but whether the system handles real lending’s variety and scales without breaking.

We built that system. The results at SME Capital prove it works. Our agentic loop delivers the reliable spreading, validation, and insights that make this possible.